- The core banking system sucks.

- It sucks for everyone, but it sucks more if you are poor or live under a dictatorship.

- Technology allows us to build a better core banking model.

- By core banking, I mean deposits and loans existing in the real economy. Not just transferring value between users or creating synthetic financial products.

- Here is the formula for a better banking model: matched funding (deposits-loans) + insurance + blockchain technology.

- This will help reduce inequality, combat authoritarianism and diminish excess variance in the business cycle.

- In this coming struggle, you are either with the spirit of our better human values epitomized by Satoshi Nakamoto or you are with the big banks.

The problem

Billions of people live in a darkness that a better banking model can lighten.

According to the World Bank, approximately 3.5 billion people live in poverty and don’t have a savings account at a bank. This

means that a couple in Mozambique has no savings mechanism that could

help them in their hope to educate their daughters. Like many, their

only choice is to operate in cash, even though the father has a job.

The Human Rights Foundation estimates that 4 billion people live under authoritarian governments. This

means that a young man studying in Vietnam keeps quiet about the

malignancies he sees in the system. He does this because he dreams of

getting married and to get the girl he needs a house and to get the

house he needs a mortgage from the state bank.

Consider this reality closer to home:

“Bank of

America will charge low-income customers $12 per month for their

checking accounts unless they have a $1,500 account balance.”

@laura_nelson, Twitter, 2018

“Finally, a bank with some fresh ideas on how to make poor people poorer.”

@kashanacauley, Twitter, 2018

Let’s see what binds these people together

A secure savings account is foundational

to a full life, a life where the individual can express the truth as

they see it and also participate in the natural uplift of the real

economy. It is the solid ground that allows us to formulate our own

thoughts without outside influence and provide a better future for our

families.

Although we tend to overlook such basics

in the West, the virtues arising from secure savings accounts are

indispensable to higher-order democratic structures. This can be seen

graphically, as a kind of Maslow hierarchy of needs.

This flows not from elections at the top, but from secure savings accounts at the bottom, plugged into the real economy. Where people have the independence to come up with their own opinions without coercion and are able to share in the productivity of the economy, societies flourish.

So, what binds those living in

authoritarian countries, the unbanked in Africa, and the financially

excluded in America together? They

are all missing the secure, productive savings account foundation

needed as a defense against the related evils of authoritarianism and

inequality.

What would core banking look like, if it were truly to serve society?

A core banking system built to serve society would have the values set out below.

Today’s fractional reserve banking system

is designed for the benefit of the few rather than the many. The very

nature of fractional reserve banking is incompatible with a truly

healthy society.

Why does the current core banking system suck?

Our banking system originates from

precious metal guilds in the Middle Ages. Deposited gold mainly

represented value that had already been created in the economy. These

guilds developed the concept of issuing paper IOUs against the deposited

gold. As not all depositors typically demanded their gold back at the

same time, this led the depositories to issue more paper IOUs for making

loans than the gold that they held. They retained a “fraction” of the

gold, in case a merchant needed physical gold. These depositories

evolved into today’s banks, whose core model is based on the same

fractional reserve concept.

This core banking system is inherently dishonest. At its heart are three fundamental lies that pervert society and the economy:

- The bank will tell you that the money you deposit belongs to you. In fact, legally the money becomes the property of the bank. In law, you are an unsecured creditor to them. In return, the bank gives you an IOU, called a deposit account. The deposited money is recorded as an asset on their balance sheet and deposit accounts are recorded as their liability to you.

- The bank will tell you that “your” money is safely held at the bank. In fact, the bank holds only a fraction and then loans the rest of it out. If you want more than this fraction of your money back, the bank takes it from elsewhere.

- The bank will tell you that your funds are “insured” by the government, up to a certain amount. In fact, there is no government insurance fund that corresponds to these deposit amounts. It isn’t insurance; it is a government undertaking, in a failure situation, to print more money to give to the banks so that they can repay their liability to you.

Banking’s greatest deception is

that the power of money creation is mainly in the hands of private

commercial banks, not the state. The Federal Reserve doesn’t create most

of the money in the United States; large American banks do, through the

loan-deposit account process. Since both paper money and bank created

money have purchasing power, they are both officially considered money.

There are two main reasons why this core

banking system sucks: it leads to inequality in society and it’s

dangerous for the economy.

Inequality in society

The banking system uses the funds of

depositors as their own to make high returns, driven by profits on

loans. Deposits and loans are the core of banking and are exceptionally

profitable given the risk assumed. The system essentially is a mechanism

for taking a little bit from everyone and channeling it to owners, who

are disproportionately the 1% of society. All depositors are

disadvantaged by their exclusion from the rewards of the natural

productivity of the economy, whether they are middle-class savers in

America or a wealthy family office in Switzerland or a corporation in

Japan.

In addition, the biases in the lending

process, driven by human preferences that manifest themselves

technically in the debt service coverage ratio or interest rate on

loans, inevitably favor in-groups over out-groups. This bias is

institutional, exacerbated by the structural nature of fractional

reserve banking.

Further, the current banking system has

completely failed the poor, in developed and developing countries. In

general, they remain excluded from being able to participate

meaningfully in the financial system. Those who do participate have few

means to share in the benefits of economic growth that could help lift

them out of poverty.

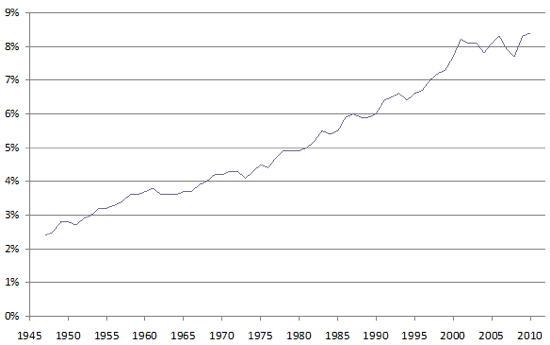

Here are two graphs from the United States that illustrate how the current banking system contributes to inequality.

Share of the finance and insurance sectors in the United States since WWII (% of GDP)

Source: US Bureau of Economic Analysis, 2015

This

graph shows that lower- and middle-class income has been declining over

the same period. It is similar in most developed countries.

When you put the two charts on top of

each other, you have a clue as to where this income has gone over the

past decades. It has gone (partially) to the financial sector. It has

also gone to other areas, like globalization, but a large part of the

benefits of the economy has been captured by big banks at the expense of

the lower and middle classes.

Dangerous for the economy

Bank credit money creation is the largest source

of funds for loans in the economy. There are three uses of loans: (1)

for productive economic activities, (2) for time shifting of

consumption, or (3) for asset purchases. The first two rely on future

cashflows for repayment. The third, asset loans, rely on the future

valuation of those assets.

When bank-created money is used for asset

loans, it leads to upward valuation levels that create excess variance

in the business cycle. When asset prices reset to lower levels, this

causes recursive destruction of both the loan value (on the asset side)

and the bank-created credit money (on the liabilities side). It is this

process that is mainly responsible for excess downward variance in the

business cycle. Bank money creation used for asset loans explains most

of the booms and busts in the economy. This can be seen in the graph

below, with recessions in grey.

Source: Federal Reserve Bank of St. Louis. Data from 1 January 1918 to 30 September 2018

This

graph shows that recessions are a regular occurrence as part of a

fractional reserve banking system; they are an inherent part of a bank

money creation model.

The main objectives for a central bank

that oversees the fractional reserve banking system are price

stability and employment. Let’s have a look at a chart of the purchasing

power of the US dollar since the inception of the Federal Reserve to

the end of 2017, to see if the price has stayed stable.

OK, so the product has lost 95% of its value and you wanted it to be stable. That isn’t so great on the CV. But,

it has outperformed almost every other nation state currency and that

is why it is the global reserve currency today. The only other money

product that has done better is gold, which somehow has held its value

since Neolithic times.

Now you understand the dangerous effect

of being able to print more paper money versus a monetary asset with a

fixed (or slow growth) supply. Even worse, the banking system creates

more money than the state. Further, the rewards of banking accrue only

to bank owners and employees while the risks of their actions are borne

by society as a whole.

This is our modern fractional reserve

banking system. It is not at all capitalist; it is more like a closed,

medieval guild system, and it will always foster inequality and exclude

out-groups by its very nature. It is as destructive as it is dishonest.

It is about as far away from the concept of value, and from our better

human values, as you can get.

What is the solution?

Until recently, there was no feasible alternative to a centralized banking system that favored the few at the top.

Then, in 2009, Satoshi Nakamoto created a

system of money that corresponds to how humanity exchanged value for

most of our history, directly, before the rise of modern banks. The

implications are spectacular: you can now trust exchanging value with

another person or institution directly, globally, even if you don’t know them.

As the crypto system is based on radical

transparency and honesty, as well as the inability for anyone to create

money; it is antithetical to the fractional reserve banking system. It

is global and impervious to authoritarian control.

The solution to the fractional reserve

banking model is to use Satoshi’s technology to radically rethink how

core banking could actually be used to benefit society. Here are some

ideas, based on the two values identified above.

This should lead to banking being

unbundled, like many other industries. The base layer will be core

banking. Other banking services can be add-ons; the consumer can choose

the best ones for them without having to accept an entire package and

without the silo inefficiencies that exist today.

Banking should function more like a

utility and stop eating such a large share of the economy. Returns

should flow to depositors. In the future, bankers should be more like

servants of other people’s money than arrogant masters of the universe.

A better banking model

The new bank should do what technology does best: attack high and unjustified margins and share the benefits with users.

Here is the formula for a better core banking model:

Better banking = matched funding (deposits-loans) + insurance + blockchain technology

This new bank should have a narrow focus: matching deposits to loans, using sophisticated matching software.

To provide security for depositors, the loans and deposits should both be insured. This

is well possible and insurance is vital in providing trust to

depositors. Banks rely on their brand name and government deposit

insurance for trust. For a new bank, providing genuine deposit insurance

would neutralize these advantages.

The new bank should run on blockchain

architecture, principally the bitcoin blockchain. As core banking

requires identification, there will need to be a permissioned layer,

best built using open-source Hyperledger software. This should have

safeguards to ensure that control remains with the user and not with the

bank. Both the core banking function and the insurance element should

move to as decentralized a model as possible and basic functionality

should be encapsulated in smart contracts, not left to management

discretion.

There is no reason that ownership of the

new bank should only be in the hands of a few shareholders. All

depositors contribute to success and their contribution to making the

pie bigger for everyone should be rewarded with an amount of equity

tokens in the new bank over time. All users could be owners.

There is also no reason for the new bank

to report only selective information and only a few times a year. A new

model of radical openness that reported daily and hashed key information

to the blockchain would inspire confidence in users.

The new bank should explicitly be founded

on the idea of making the world a better place. A good example is for

the new bank to have a policy of donating a set amount of profits to

local charities, say 10%.

What is not a better core banking model

The fractional reserve banking model sucks. Putting this model on a blockchain architecture doesn’t make it suck any less.

Fintechs, challenger banks, crypto banks

typically don’t do core banking and are not a new model; they are just a

lesser evil. The JPM coin framework is not crypto, not a new model and

not a lesser evil.

Now is the hour to choose a side

It is time for a better banking model,

for a better world. The cornerstone of this new relationship must be a

secure savings account that guards against authoritarianism and allows

users to participate in the productivity of the real economy.

This is a rare moment in history to

create a new model, which won’t last forever. Most technology has

in-built authoritarian tendencies. Satoshi’s invention is an exception,

an opportunity to re-create a system without centralized control. The

crypto system will only change the world if it can connect in a

meaningful way to the real economy and deliver tangible value to users

in a simple offer.

The fight to establish a better banking

model will be demanding, against an entrenched enemy. However, the

market is enormous and the financial rewards compelling. The possibility

of making a better, healthier society should lead us on. If the idea of

a better banking model speaks to you, and you are willing to get your

hands dirty, join us.

Source link: dailyhodl.com

0 Comments